FreedX Backtest Plus█ Our new FreedX Backtest PLUS template enhances TradingView backtesting with smart features like Mean Reversion, Flexible Volatility, Liquidation Filter, and Better Trend Filtering, making strategies more effective. It lets users set up automated alerts easily. This guide explains how to make the most of these improved features.

The Trading Date Settings feature in our TradingView script allows you to refine their backtesting parameters by specifying trading dates and hours. This feature enhances the accuracy of the backtest by aligning it with specific time frames and days, ensuring that the strategy is tested under relevant market conditions.

Features:

⚙️ Enable Trading Between Specific Dates:

🎯 Purpose:

→ Allows you to limit the backtesting of their strategy to a specific date range.

💡 How to Use:

→ Input the Start Date and End Date for the backtest period.

→ The script will execute the strategy only within this specified date range.

⚙️ Enable Trading Between Specific Hours:

🎯 Purpose:

→ Allows you to limit the backtesting of their strategy to a specific hour range.

💡 How to Use:

→ Input the start and end hour for in Trading Session section.

→ The script will execute the strategy only within this specified hour range.

⚙️ Enable Trading on Specified Days of the Week:

🎯 Purpose:

→ Gives you the option to conduct backtesting on selected days of the week, tailoring the strategy to particular market behaviours that may occur on these days.

💡 How to Use:

→ Select the days of the week for the backtest.

→ The script will activate the trading strategy only on these chosen days.

█ BUY/SELL TRIGGER SETTINGS

The Buy/Sell Trigger Settings feature is designed to provide users with flexibility in defining the conditions for 'LONG' and 'SHORT' signals based on various indicator types. This customization is crucial for tailoring strategies to different trading styles and market conditions.

Features:

⚙️ Single-Line Plotted Indicators :

🎯 Purpose:

→ Enables you to select a single-line plotted indicator as a source for backtesting. You can define specific levels to trigger 'LONG' or 'SHORT' signals.

💡 How to Use:

→ Choose a Single-Line Plotted indicator as the source.

→ Set the top and bottom levels for the indicator.

→ The script triggers 'LONG' signals at the bottom level and 'SHORT' signals at the top level.

⚙️ Two-Line Plotted Indicators :

🎯 Purpose:

→ Allows backtesting with two-line cross plot sources. Signals are generated based on the crossover of these lines.

💡 How to Use:

→ Select two lines as 'Source 1' and 'Source 2' for the indicator.

→ The script triggers a 'LONG' signal when 'Source 1' crosses above 'Source 2'.

→ Conversely, a 'SHORT' signal is triggered when 'Source 2' crosses above 'Source 1'.

⚙️ Custom Signals :

🎯 Purpose:

→ This setting enables users to define their own criteria for LONG, SHORT, and CLOSE signals based on custom indicator outputs.

💡 How to Use:

→ Select the custom source for your signals.

→ Define the output values that correspond to each signal type (e.g., “1” for 'LONG', “-1” for SHORT, and “0” for CLOSE).

→ The script will trigger signals according to these custom-defined values.

█ TP/SL SETTINGS

The TP/SL (Take Profit/Stop Loss) Settings feature is designed to give users control over their profit securing and risk mitigation strategies. This feature allows for setting custom TP and SL levels, which can be critical in managing trades effectively.

Features:

Custom TP/SL Levels for Long/Short Signals:

🎯 Purpose:

→ Enables users to set specific percentage levels for Take Profit and Stop Loss on long and short signals.

💡 How to Use:

→ In the TP/SL Settings, input the desired percentage for Take Profit (TP) and Stop Loss (SL).

→ For example, to secure a profit at a 10% price increase on LONG signals, set the “Long TP Percentage” to “10”.

█ STRATEGY SETTINGS

Strategy Settings provide a range of options to customize the trading strategy. These settings include leverage, position direction changes, and more, allowing users to tailor their strategy to their risk tolerance and market view.

Features:

⚙️ Enable Reverse Position:

🎯 Purpose:

→ Automatically closes a current position and opens a new one in the opposite direction upon detecting a signal for a market trend change.

🎯 Example:

→ If a LONG signal is received while in a SHORT position, the script will close the SHORT position and open a LONG position.

💡 How to Use:

→ Activate this feature in the Strategy Settings.

⚙️ Enable Spot Mode:

🎯 Purpose:

→ Disables short orders, using short signals only for closing long positions.

💡 How to Use:

→ Select the 'Spot Mode' option in the Strategy Settings.

⚙️ Enable Invert Signals:

🎯 Purpose:

→ Inverts all indicator signals, changing LONG signals to SHORT and vice versa.

💡 How to Use:

→ Opt for the 'Invert Signals' feature in the Strategy Settings.

⚙️ Enable Trailing Stop:

🎯 Purpose:

→ Triggers a trailing stop order on the exchange instead of a standard stop market order.

☢️ Caution:

→ The backtesting of this feature on TradingView may not accurately reflect actual strategy performance due to discrepancies between TradingView and exchange mechanisms.

💡 How to Use:

→ Select 'Trailing Stop' in the Strategy Settings.

⚙️ Enable Realistic TP & SL:

🎯 Purpose:

→ Goal is protect the user from unrealistic stop loss and take profit prices in live exchange trading conditions.

→ That feature continuously checks the take profit, stop loss and move stop loss prices to prevent unrealistic values. It changes their values according to (minimum realistic percent %)

💡 How to Use:

→ Select 'Enable Realistic TP & SL' in the Strategy Settings. Write min allowed percents.

█ LIMITER SETTINGS

Limiter Settings provide a range of options to customize the trading strategy. These settings include drawdown limits,contract limit, tradable ratio, for allowing users to tailor their strategy to their risk tolerance and market view.

⚙️ Leverage :

🎯 Purpose:

→ Allows users to apply leverage to their trades.

☢️ Caution:

→ High leverage can significantly increase the risk of liquidation.

→ High leverage and a high stop-loss price may override your fixed stoploss percentage, adjusting the stop-loss to the liquidation price.

💡 How to Use:

→ Set the desired leverage ratio in the Strategy Settings.

⚙️ Drawdown Limit:

🎯 Purpose:

→ Sets a maximum drawdown limit, automatically halting the strategy if this limit is reached, thereby controlling risk.

💡 How to Use:

→ Input the maximum drawdown limit (default: 100, min: 0, max: 100).

⚙️ Contract Limit:

🎯 Purpose:

→ Sets a maximum contract limit, beyond which the compound effect cannot be used. This is important to prevent market manipulation through large-volume orders.

💡 How to Use:

→ Input the maximum contract limit (min: 0).

⚙️ Tradable Ratio:

🎯 Purpose:

→ Sets a tradable ratio, it uses that ratio calculating entry cost for position. Main purpose is cash-out and cash-in according to balance change.

💡 How to Use:

→ Input the tradable ratio percent (default: 98, min: 0.1, max: 100).

█ CASH-OUT SETTINGS

Cash-Out Settings offer a money-saving mechanism that prevents entering positions with the entire balance due to cashed-out funds. It functions with a webhook alerts, but the 'Override Allocation %' option must be enabled.

⚙️ Cash-out Threshold %:

🎯 Purpose:

→ It is cash-out mechanism, it saves money with a target threshold.

💡 How to Use:

→ Input the threshold (min: 0).

⚙️ Cash-out Per Profitable Trades %:

🎯 Purpose:

→ It is cash-out mechanism, it saves money from every trade with a percent like commission.

💡 How to Use:

→ Input save percent% (min: 0).

█ ADAPTIVE VOLATILITY STRATEGY SETTINGS

Advanced Strategy Settings offer sophisticated methods for managing Stop Loss (SL) and Take Profit (TP) using the Average True Range (ATR). These settings are ideal for traders who want to incorporate volatility into their exit strategies.

Features:

⚙️ Enable ATR Stop Loss:

🎯 Purpose:

→ Automatically sets the Stop Loss price using the Average True Range at the time of entry.

💡 How to Use:

→ Activate 'ATR Stop Loss' to have the SL price calculated based on the current ATR.

⛓ Enable ATR Trailing Stop:

→ Dynamically updates the Stop Loss price with each new bar, according to the Average True Range.

→ Activate 'ATR Trailing Stop'.

→ Set the ATR Period to define the number of bars for ATR calculation.

→ Adjust the ATR SL Multiplier to determine the stop loss distance.

→ Modify the ATR TP Multiplier for setting the take profit distance.

⚙️ Enable ATR Take Profit:

🎯 Purpose:

→ Sets the Take Profit price based on the Average True Range at the time of entry.

💡 How to Use:

→ Choose 'ATR Take Profit' for TP price determination using ATR.

⚙️ Enable ATR Limit Entry:

🎯 Purpose:

→ Trade can not open in candle close price. Price should hit target price that based on average true range value.

💡 How to Use:

→ Choose 'ATR Limit Entry' for entry price determination using ATR.

⛓ Enable ATR Limit Entry Trailing Price:

→ Dynamically updates the entry price with each new bar, according to the Average True Range.

→ Activate 'ATR Limit Entry Trailing Price'.

→ Set the ATR Period to define the number of bars for ATR calculation.

→ Adjust the ATR SL Multiplier to determine the stop loss distance.

→ Modify the ATR TP Multiplier for setting the take profit distance.

█ TREND FILTERING SETTINGS

Trend Filtering Settings are designed to align trading strategies with the prevailing market trend, enhancing the precision of trade entries and exits. These settings utilize moving averages for trend analysis and decision-making.

Features:

⚙️ Enable Moving Average Filtering:

🎯 Purpose:

→ Limits trades based on moving average trends, blocking short trades in an uptrend and vice versa.

💡 How to Use:

→ Enable 'Trend Filtering'.

→ Set Fast and Slow MA Lengths for trend analysis.

→ Select the Timeframe for moving averages.

→ Choose the Moving Average Type for trend filtering.

🎯 Note:

→ Be cautious with timeframe selections; lower timeframes than the base may cause inconsistencies.

⛓ Exit on Trend Reversal:

→ Automatically closes a position when a market trend reversal is detected.

→ Turn on 'Exit on Trend Reversal' in the settings.

⛓ Ignore Counter Signals:

→ Ignores counter signals during trending market way.

→ If the trend way is long. All short signals will ignore and vice versa.

⛓ Enable Drawing On Chart:

→ Visually represents the trend filter directly on the chart for easy reference.

→ Activate 'Drawing On Chart' to see the trend filter overlaid on the trading chart.

⚙️ Enable Adx Filtering:

🎯 Purpose:

→ Limits trades based on adx value, blocking trades if trend strength is not enough or vice versa for invert mode.

💡 How to Use:

→ Enable 'Adx Filtering'.

→ Set Smoothing and Lengths for adx trend analysis.

→ Select level barrier for trend strength.

⚙️ Enable Custom Filtering:

🎯 Purpose:

→ Limits trades based on custom sources, blocking trades according to custom trades.

💡 How to Use:

→ Enable 'Custom Filtering'.

→ Select fast source.

→ Select slow source.

→ Enable lag mode.

█ MEAN REVERSION FILTERING SETTINGS

Mean Reversion Filtering Settings are designed to align trading strategies during accumulation market conditions. They set a distance from a line to permit trading. The purpose is to ensure that when the price strays too far from the mean line, it should revert back. In accumulation markets, price movements are generally horizontal. In such situations, mean reversion will operate like a grid, enabling profitable trades with low drawdown. However, when the market structure begins to trend, mean reversion filters may not be as profitable as in accumulation markets. For instance, let's say the price is rising and we are shorting the market until it reaches the mean price line. As the price goes up and the mean also rises, we will end up closing the position at a higher price, rendering the mean reversion system non-profitable. Therefore, consider this filter wisely; greater distances might work better in trending markets.

Features:

⚙️ Enable Kairi Filter:

🎯 Purpose:

→ Blocks trades based on distance percent between price and moving average.

💡 How to Use:

→ Enable 'Kairi Filter'.

→ Set Length and Distance Percent.

⛓ Enable Trend Drawing On Chart:

→ Visually represents the trend filter directly on the chart for easy reference.

→ Enable 'Drawing On Chart' to see the allowed regions overlaid on the trading chart with arrows.

⚙️ Enable VWAP Filter:

🎯 Purpose:

→ Blocks trades based on distance percent between price and volume weighted average price.

💡 How to Use:

→ Enable 'VWAP Filter'.

→ Set Timeframe as minutes and distance as percent.

⛓ Exit on Crossing with VWAP:

→ Automatically closes a position when the closing price of a candle crosses the VWAP.

→ Choose "Enable", 'Exit on Crossing with VWAP' in the settings.

⛓ Enable Drawing On Chart:

→ Visually represents the trend filter directly on the chart for easy reference.

→ Enable 'Drawing On Chart' to see the allowed regions overlaid on the trading chart with arrows.

█ LIQUIDATION FILTER SETTINGS

Liquidation filter compares the volume data of futures and spot markets.

Large differences in volume indicate unexpected market conditions, such as massive trading activities, which may signal liquidations.

Features:

⚙️ Enable Liquidation Filter:

🎯 Purpose:

→ Blocks trades based on extra ordinary volume differences in spot and futures market.

💡 How to Use:

→ Enable 'Liquidation Filter'.

→ Set behavior to react during that market conditions.

→ Set base amount to filter volume. This amount changes according to timeframe, you should find right amounts.

→ Liquidation candle count means, it is sum of liquidated candle count in last 20 bars.If you set 0, it means feature is disabled.

→ Detection, try to select the spot and perpetual symbols automatically, symbol names varies, it do not support all symbols, you should choose manually in that situation.

█ AUTOMATED ALERT SETTINGS

Automated Alert Settings are designed to integrate your TradingView script with webhook alerts. These settings allow for enhanced strategy execution and management.

Features:

Enable Webhook Alerts:

🎯 Purpose:

→ Trigger BUY, SELL, CHANGE_DIRECTION or MOVE_STOP_LOSS .

💡 How to Use:

→ Enable 'Webhook Alerts' in the settings.

→ Enter your Strategy Key.

→ Optionally, activate 'Override Allocation Percentage' to bypass the preset allocation percentage.

☢️ Caution:

→ Overriding the allocation percentage may result in trade entry errors due to misalignment between entry cost and available balance.

Enable Custom Alerts:

🎯 Purpose:

→ User can produce unique messages for different purposes.

💡 How to Use:

→ Enable 'Custom Alerts' in the settings.

→ Enter your message format type.

█ DEBUGGING SETTINGS

Debugging Settings are crucial for users who want to analyze and optimize their strategies. These settings provide tools for visualizing alerts on charts and accessing detailed data outputs.

Features:

⚙️ Enable Alert Plotting:

🎯 Purpose:

→ Allows users to visualize trading alerts directly on the chart, aiding in strategy analysis and refinement.

💡 How to Use:

→ Activate 'Alert Plotting' to draw alerts on the chart.

☢️ Caution:

→ It is recommended to disable this feature when creating actual trading alerts, as it can cause latency in signal processing.

⚙️ Enable Debugger Mode:

🎯 Purpose:

→ Facilitates strategy debugging by providing detailed data output in the TradingView Data Window.

💡 How to Use:

→ Turn on 'Debugger Mode' to access real-time data and metrics relevant to your strategy.

⚙️ Enable Table:

🎯 Purpose:

→ Facilitates strategy debugging by providing detailed data output in the TradingView Table on chart.

💡 How to Use:

→ Turn on 'Table' to access last closed candle data and metrics relevant to your strategy.

█ ADDITIONAL SETTINGS

⚙️ Enable Bar Magnifier

⚙️ Enable Using standard OHLC

Cerca negli script per "take profit"

Contrarian DC Strategy - w Entry SL Pause and TrailingStopDonchian Channel Setup:

The strategy uses a tool called the Donchian Channel. Imagine this as two lines (bands) on a chart that show the highest and lowest prices over a certain number of past trading days (default is 20 days).

There's also a centerline, which is the average of these two bands.

Entry Conditions for Trades:

Buying (Going Long): The strategy considers buying when the price touches or falls below the lower band of the Donchian Channel. However, this only happens if there has been a pause after a previous losing trade. This pause is a number of candles where no new trades are taken.

Selling (Going Short): Similarly, the strategy considers selling when price reaches or exceeds the upper band of the Donchian Channel. Again, this is subject to a pause after a losing trade.

Stop Loss and Take Profit:

Each trade has a "Stop Loss" and "Take Profit" set. The Stop Loss is a preset price level where the trade will close to prevent further losses if the market moves against your position. The Take Profit does the same but locks in profit if the market moves in your favor.

The Stop Loss is set based on a percentage of the price at which you entered the trade.

The Take Profit is determined by the Risk/Reward Ratio. This ratio helps balance how much you're willing to risk versus the potential reward.

Trailing Stop Loss:

When a trade is profitable, the strategy should involve a "Trailing Stop Loss." This means the Stop Loss level moves (or trails) the price movement to lock in profits as the market moves in your favor.

For a buy trade, if the price moves above the centerline of the Donchian Channel, the Trailing Stop Loss should be adjusted in the middle between the entry price and the centerline. Viceversa for a sell trade, it should be adjusted in the same way if the price goes below the centerline.

IMPORTANT: There's no allert for the trailing stop at the moment.

Post-Stop Loss Pause:

If a trade hits the Stop Loss (i.e., it's a losing trade), the strategy takes a break before opening another trade in the same direction. This pause helps to avoid entering another trade immediately in a potentially unfavorable market.

In summary, this strategy is designed to make trades based on the Donchian Channel, with specific rules for when to enter and exit trades, and mechanisms to manage risk and protect profits. It's contrarian because it tends to buy when the price is low and sell when the price is high, which is opposite to what many traders might do.

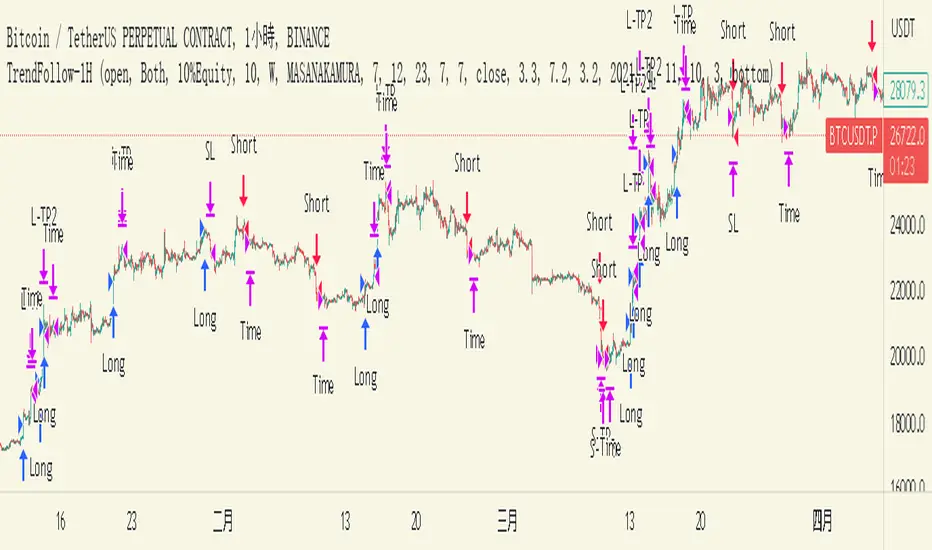

TrendFollow-1HThis is a trading strategy specially used on btcusdtperp in binance 1H chart

The most important part of this strategy is to use Support and Resistance with trading volume

Auxiliary indicators are include Directional Movement Index, trading volume, Commodity Channel Index,volume-weighted average price,Range Filter

Why is it not applicable to other trading varieties or exchanges?

Because the activity of each trading target is different from the trading volume, this strategy is very focused on the change of trading volume, so it may not be applicable to every trading variety

The idea of this strategy is to chase when the trend in the market is clear

Determine whether to break support or resistance to identify trends

But the market is full of false breakouts

Therefore, trading volume is an important indicator for judging the true and false.

Therefore, when the price breaks through support or resistance, accompanied by a huge trading volume, and forms a resonance with auxiliary indicators, the strategy will follow the trend, a time stop loss is also set. After entering the market, if there is no immediate profit to the stop profit, you will leave the market first.

But the market is always random, so the profit and loss ratio must be taken into account

Use a fixed stop loss space in exchange for a larger profit space, and ensure that the expected value is positive to make stable profits in the market

Therefore, this strategy uses 3.2% stop loss, 3.3% Take profit1 and 7.2% take profit2

About 1.5:1 profit and loss ratio to ensure positive expected value

Because the market has a clear trend only about 10% of the time

So the trading frequency of this strategy is very low

According to the backtest of up to 2021-01-01 till now , it takes about 5 days to make a transaction

User can choose their own leverage to obtain higher returns. But be sure to prioritize risk.

In order to prevent you from using this strategy without knowing it, the trading date of this strategy is only executed until the release date, and positions will not be opened and closed for subsequent markets.

You can contact me if you want to know more about this strategy

這是專門用於幣安1H圖表中btcusdtperp的交易策略

本策略最重要的部分是將支撐和阻力與交易量一起使用

輔助指標包括ADX,成交量,CCI,VWAP,Range Filter等

為什麼不適用於其他交易品種或交易所?

由於每個交易標的的活躍度與交易量不同,本策略非常注重交易量的變化,因此不一定適用於每個交易品種

這個策略的方法是在趨勢明朗的時候進行趨勢跟隨

確定是否打破支撐或阻力以識別趨勢

但市場充滿假突破

因此,成交量是判斷真假的重要指標。

當價格突破支撐位或阻力位,伴隨著巨大的成交量,並與輔助指標形成共振時,策略會順勢而為,同時設置時間止損。進場後,如果沒有立即獲利到止盈,就離場。

但市場總是隨機的,所以必須考慮盈虧比

用固定的止損空間換取更大的盈利空間,保證預期值為正,才能在市場中穩定獲利

因此,該策略使用 3.2% 止損、3.3% 止盈1 和 7.2% 止盈2

約1.5:1盈虧比,確保正期望值

因為市場只有大約 10% 的時間有明顯的趨勢

所以這個策略的交易頻率很低

根據2021-01-01至今的回測,交易頻率大約5天一次

用戶也可以選擇適合自己的槓桿以獲得更高的收益。但一定要優先考慮風險。

為防止您在不知情的情況下使用本策略,本策略的運行交易的日期僅至2023-05-30止,後續日期將不開倉和平倉。

如果您想了解更多有關此策略的信息,可以聯繫我。

Baseline Cross Qualifier Volatility Strategy with HMA Trend BiasFor trading ES on 30min Chart

Trading Rules

Post Baseline Cross Qualifier (PBCQ): If price crosses the baseline but the trade is invalid due to additional qualifiers, then the strategy doesn't enter a trade on that candle. This setting allows you override this disqualification in the following manner: If price crosses XX bars ago and is now qualified by other qualifiers, then the strategy enters a trade.

Volatility: If price crosses the baseline, we check to see how far it has moved in terms of multiples of volatility denoted in price (ATR x multiple). If price has moved by at least "Qualifier multiplier" and less than "Range Multiplier", then the strategy enters a trade. This range is shown on the chart with yellow area that tracks price above/blow the baseline. Also, see the dots at the top of the chart. If the dots are green, then price passes the volatility test for a long. If the dots are red, then price passes the volatility test for a short.

Take Profit/Stoploss Quantity Removed

1 Take Profit: 100% of the trade is closed when the profit target or stoploss is reached.

2 Take Profits: Quantity is split 50/50 between Take Profit 1 and Take Profit 2

3 Take Profits: Quantify is split 50/25/25.

Stratgey Inputs

Baseline Length

37

Post Baseline Cross Qualifier Enabled

On

Post Baseline Cross Qualifier Bars Ago

9

ATR Length

9

Volatility Multiplier

0

Volatility Range Multiplier

10

Volatility Qualifier Multiplier

2

Take Profit Type

1 Take Profit

HMA Length

11

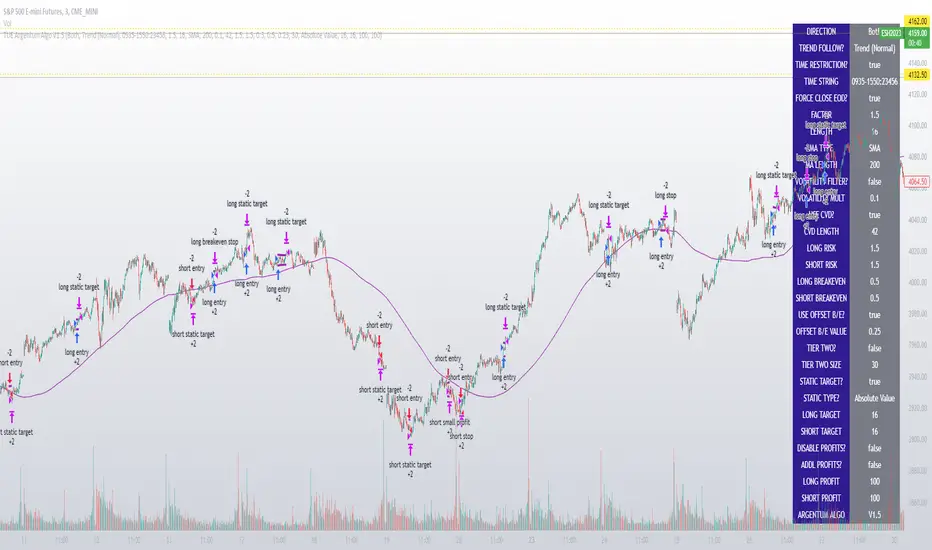

TUE Argentum Algo V1This algorithm is designed to look trend for opening conditions, apply various filters including volume and volatility, then determine stop outs, break evens, and take profits.

The algorithm uses proprietary math based on the concepts of volatility, standard deviations, average true ranges, and volume to help determine trend. You can filter based on cumulative volume delta, volatility, and moving average based trend. It includes settings for either trend following or contrarian trades, and the ability to go long, short, or both.

The take profit areas are based on proprietary math that help find peaks and valleys. You can adjust the size of the take profits as a percentage of the position, change to static take profits (i.e. take profit in 16 ticks), or use both. You can also disable them and use the natural closing conditions of the trades (detection of trend change in the opposite direction).

Our algo works in any market and will allow user to adjust input settings to be used on any ticker they'd like. It is built as a strategy so you can back test on any ticker to find the exact right settings to dial it in and then switch to live trading mode to see signals. Can be used for day trades or swing trades.

Automated Trading

This algo has been tested and certified to work for automated trading.

Works on Forex

It's confirmed to work on forex so you can trade that market.

Gets you into long successful trades, and gets out of poor ones quickly

It keeps you in the long trades taking small profits along the way, but cuts losers quickly in comparison. This style leads to a high profit factor.

It looks at many variables so you don't have to

- Uses trend analysis for opening/closing conditions.

- It measures the strength of trends to help determine if it should enter or not.

- It uses volume, if the user wants, to help filter entries. The volume calculation is based off of my proprietary cumulative volume delta indicator and helps find if the volume is moving long or short.

- It uses proprietary take profit math to help find peaks and valleys to peel off profits. It is based on the changes in momentum of the underlying.

- It allows for stop outs and break evens based on volatility so they'll always adjust with the movement of the underlying ticker (see the blue lines above and below the opening in the chart).

- It allows for offset break evens to keep a portion of the profit.

Strategy for the Algo

Included so you can understand how to trade with it.

ONE: After loading this strategy onto a ticker turn off volume if it's a ticker with no volume , set the dates at the bottom to when the stock is active (you want to start backtesting when a stock started trading like it trades currently).

TWO: From there adjust the short term trend settings to find the highest win rate and profit factor.

THREE: Then adjust the volume length to find the highest win rate and profit factor. It's important while doing these that you pay attention to a smooth upward equity curve.

FOUR: After this has been done now adjust the long and short risk multipliers. This determines your stop out.

FIVE: Then adjust breakeven multipliers - this is the level at which it changes to a breakeven stop out instead of the previous one. You can also set an offset to keep a small part of the profit.

SIX: Finally adjust the take profit sizes.

SEVEN: Once this is all done go back through the list and adjust up and down by one or two clicks and see if a better curve can be obtained. Very frequently long and short trades have different settings.

EIGHT: When you are finished save the settings in a custom indicator template and put it with it's own chart.

Additional

The settings shown on screen are not the default settings, but are settings chosen for this ticker and timeframe based on the process above. Nearly every ticker and timeframe will require adjustment from default, that's why the algorithm is built to be highly flexible. It can fit any ticker and timeframe, as well as market environment.

This particular setup has the algo running a scalping program on ES 3 min with a 16 tick static target. This algorithm can be set up as a scalper, or used to day trade more regularly. It can also swing trade.

As shown here the algo includes $1.25 of commissions and 1 tick of slippage on all orders (about our average for automated trading on ES).

TUE ADX/MACD Confluence Algorithm V1This algorithm is designed to look at the ADX/MACD confluence for opening conditions, apply various filters including volume and volatility, then determine stop outs, break evens, and take profits.

The ADX and MACD confluence can be a powerful predictor in stock movements. Both of these indicators find trend but do it in different ways. When they're combined they have a high success rate of finding openings. That's done by finding the bar in which both show the same direction - that bar is the beginning of the confluence. I have a free indicator called the TUE ADX/MACD Confluence that you can use to see this in action.

This script will help you find those confluences in an easy to understand manner. It will open a trade on a detected confluence, using the rest of the variables available in the algorithm as filters. You can filter based on cumulative volume delta, volatility, and trend. It includes settings for either trend following or contrarian trades, and the ability to go long, short, or both.

It includes Buy and Sell signals for detected confluences, and will show colored candles to help you determine when to exit a trade if you don't want to follow the included take profit areas. When the candles turn to white that means the detected confluence is no longer in play. The Buy and Sell signals will display on the first occurrence of each confluence.

The take profit areas are based on proprietary math that help find peaks and valleys. You can adjust the size of the take profits as a percentage of the position, change to static take profits (i.e. take profit in 16 ticks), or use both. You can also disable them and use the natural closing conditions (reversal of MACD/ADX confluence).

Our algo works in any market and will allow user to adjust input settings to be used on any ticker they'd like. It is built as a strategy so you can back test on any ticker to find the exact right settings to dial it in and then switch to live trading mode to see signals. Can be used for day trades or swing trades.

Automated Trading

This algo has been tested and certified to work for automated trading.

Works on Forex

It's confirmed to work on forex so you can trade that market.

Gets you into long successful trades, and gets out of poor ones quickly

It keeps you in the long trades taking small profits along the way, but cuts losers quickly in comparison. This style leads to a high profit factor, as you can see over 3.0 in the included ES 3 Min chart.

It looks at many variables so you don't have to

- Uses ADX/MACD confluence for opening/closing conditions.

- It uses volume, if the user wants, to help filter entries. The volume calculation is based off of my proprietary cumulative volume delta indicator and helps find if the volume is moving long or short.

- It uses proprietary take profit math to help find peaks and valleys to peel off profits. It is based on the changes in momentum of the underlying.

- It allows for stop outs and break evens based on volatility so they'll always adjust with the movement of the underlying ticker (see the blue lines above and below the opening in the chart).

- It allows for offset break evens to keep a portion of the profit.

Strategy for the Algo

Included so you can understand how to trade with it.

ONE: After loading this strategy onto a ticker turn off volume if it's a ticker with no volume , set the dates at the bottom to when the stock is active (you want to start backtesting when a stock started trading like it trades currently).

TWO: From there adjust the ADX/MACD to find the highest win rate and profit factor.

THREE: Then adjust the volume length to find the highest win rate and profit factor. It's important while doing these that you pay attention to a smooth upward equity curve.

FOUR: After this has been done now adjust the long and short risk multipliers. This determines your stop out.

FIVE: Then adjust breakeven multipliers - this is the level at which it changes to a breakeven stop out instead of the previous one. You can also set an offset to keep a small part of the profit.

SIX: Finally adjust the take profit sizes.

SEVEN: Once this is all done go back through the list and adjust up and down by one or two clicks and see if a better curve can be obtained. Very frequently long and short trades have different settings.

EIGHT: When you are finished save the settings in a custom indicator template and put it with it's own chart.

Additional

The settings shown on screen are not the default settings, but are settings chosen for this ticker and timeframe based on the process above. Nearly every ticker and timeframe will require adjustment from default, that's why the algorithm is built to be highly flexible. It can fit any ticker and timeframe, as well as market environment.

Also included in the chart above is a $1.25 commission per contract, and a tick of slippage (which on average is about right for automated trading on ES).

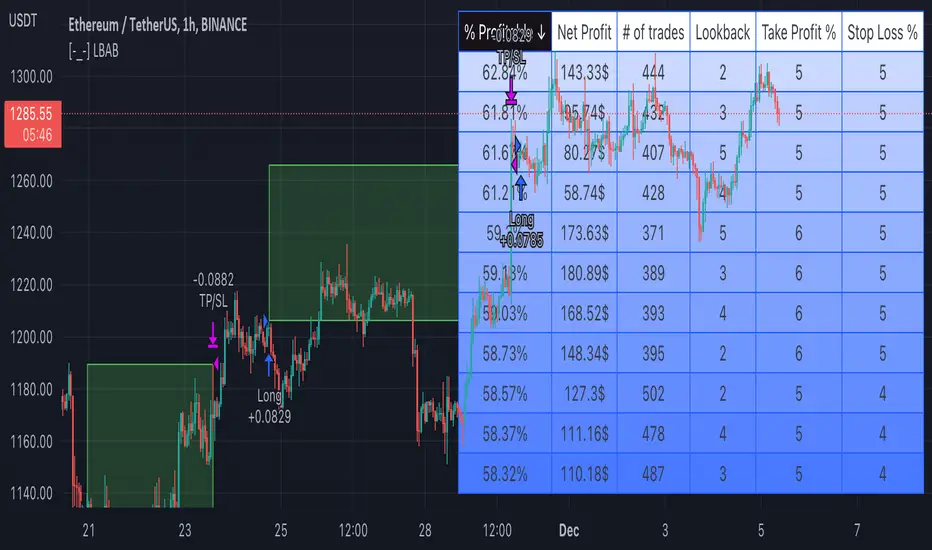

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

LuxAlgo - Backtester (S&O)The S&O Backtester is an innovative strategy script that encompasses features + optimization methods from our Signals & Overlays™ toolkit and combines them into one easy-to-use script for backtesting the most detailed trading strategies possible.

Our Signals & Overlays™ toolkit is notorious for its signal optimization methods such as the 'Optimal Sensitivity' displayed in its dashboard which provides optimization backtesting of the Sensitivity parameter for the Confirmation & Contrarian Signals.

This strategy script allows even more detailed & precise backtests than anything available previously in the Signals & Overlays™ toolkit; including External Source inputs allowing users to use any indicator including our other paid toolkits for take profit & stop loss customization to develop strategies, along with 10+ pre-built filters directly Signals & Overlays™' features.

🔶 Features

Full Sensitivity optimization within the dashboard to find the Best Win rates or Best Profits.

Counter Trade Mode to reverse signals in undesirable market conditions (may introduce higher drawdowns)

Built-in filters for Confirmation Signals w/ Indicator Overlays from Signals & Overlays™.

Built-in Confirmation exit points are available within the settings & on by default.

External Source Input to filter signals or set custom Take Profits & Stop Losses.

Optimization Matrix dashboard option showing all possible permutations of Sensitivity.

Option to Maximize for Winrate or Best Profit.

🔶 Settings

Sensitivity signal optimizations for the Confirmation Signals algorithm

Buy & Sell conditions filters with Indicator Overlays & External Source

Take Profit exit signals option

External Source for Take Profit & Stop Loss

Sensitivity ranges

Backtest window default at 2,000 bars

External source

Dashboard locations

🔶 Usage

Backtests are not necessarily indicative of future results, although a trader may want to use a strategy script to have a deeper understanding of how their strategy responds to varying market conditions, or to use as a tool for identifying possible flaws in a strategy that could potentially be indicative of good or bad performance in the future.

A strategy script can also be useful in terms of it's ability to generate more complete & configurable alerts, giving users the option to integrate with external processes.

In the chart below we are using default settings and built-in optimization parameters to generate the highest win rate.

Results like the above will vary & finding a strategy with a high win rate does not necessarily mean it will persist into the future, however, some indications of a well-optimized strategy are:

A high number of closed trades (100+) with a consistently green equity curve

An equity curve that outperforms buy & hold

A low % max drawdown compared to the Net Profit %.

Profit factor around 1.5 or above

In the chart below we are using the Trend Catcher feature from Signals & Overlays™ as a filter for standard Confirmation Signals + exits on a higher timeframe.

By filtering bullish signals only when the Trend Catcher is bullish, as well as bearish signals for when the Trend Catcher is bearish, we have a highly profitable strategy created directly from our flagship features.

While the Signals & Overlays features being used as built-in filters can generate interesting backtests, the provided External Sources can allow for even more creativity when creating strategies. This feature allows you to use many indicators from TradingView as filters or to trigger take-profit/stop-loss events, even if they aren't from LuxAlgo.

The chart below shows the HyperWave Oscillator from our Oscillator Matrix™ being used for take-profit exit conditions, exiting a long position on a profit when crossing 80, and exiting a short position when crossing 20.

🔶 Counter Trade Mode

Our thesis has always firmly remained to use Confirmation Signals within Signals & Overlays™ as a supportive tool to find trends & use as extra confirmation within strategies.

We included the counter-trade mode as a logical way to use the Confirmation signals as direct entries for longs & shorts within more contrarian trading strategies. Many traders can relate to using a trend-following indicator and having the market not respect its conditions for entries.

This mode directly benefits a trader who is aware that market conditions are generally not-so-perfect trends all the time. Acknowledging this, allows the user to use this to their advantage by introducing countertrend following conditions as direct entries, which tend to perform very well in ranging markets.

The big downfall of using counter-trade mode is the potential for very large max-drawdowns during trending market conditions. We suggest for making a strategy to consider introducing stop-loss conditions that can efficiently minimize max-drawdowns during the process of backtesting your creations.

Sensitivity Optimization

Within the Signals & Overlays™ toolkit, we allow users to adjust the Confirmation Signals with a Sensitivity parameter.

We believe the Sensitivity paramter is the most realistic way to generate the most actionable Confirmation Signals that can navigate various market conditions, and the Confirmation Signals algorithm was designed specifically with this in mind.

This script takes this parameter and backtests it internally to generate the most profitable value to display on the dashboard located in the top right of the chart, as well as an optimization table if users enable it to visualize it's backtesting.

In the image below, we can see the optimization table showing permutations of settings within the user-selected Sensitivity range.

The suggested best setting is given at the current time for the backtesting window that's customizable within the indicator. Optimized settings for technical indicators are not indicative of future results and the best settings are highly likely / guaranteed to change over time.

Optimizing signal settings has become a popular activity amongst technical analysts, however, the real-time beneficial applications of optimizing settings are limited & best described as complicated (even with forward testing).

🔶 Strategy Properties (Important)

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from strategies built are realistic.

🔶 How to access

You can see the Author's Instructions below to learn how to get access on our website.

Job's Tears - V6This strategy is based on Heikin Ashi + supertrend + DMI + RSI .

Fully functional with placing a new order, taking partial profit at the target price, taking partial profit when hit the take profit, and closing an order.

I wrote this strategy mostly in 5min timeframe.

The commission is default at 0.02% and slippage is 1.

InitCapital is 100 USD, place every new order with 20 USD, close 10 USD when hitting the target price and close 2 USD for every take profits.

No leverage is applied.

I use Heikin Ashi candle patterns to identify the buy/sell signal and supertrend to back my signal. Then I use dmi and rsi to filter out the noises.

My target is to catch a big trend, so I use a lot of take profits to maximize the potential profit.

New Short/New Long: Place a market order for a new position of 20 USD.

Target Price: Place a limited order of 10 USD at that price as soon as a new position is ordered as a basic profit in the pocket.

Take Profit: Place a market order to reduce the position by 2 USD each time.

TaoBao: Place a market order to close all remaining positions. It will only show up after hitting the target price as a way to protect our capital.

Close Short/Long: Place a market order to close all remaining positions.

[MT] Strategy Backtest Template| Initial Release | | EN |

An update of my old script, this script is designed so that it can be used as a template for all those traders who want to save time when programming their strategy and backtesting it, having functions already programmed that in normal development would take you more time to program, with this template you can simply add your favorite indicator and thus be able to take advantage of all the functions that this template has.

🔴Stop Loss and 🟢Take Profit:

No need to mention that it is a Stop Loss and a Take Profit, within these functions we find the options of: fixed percentage (%), fixed price ($), ATR, especially for Stop Loss we find the Pivot Points, in addition to this, the price range between the entry and the Stop Loss can be converted into a trailing stop loss, instead, especially for the Take Profit we have an option to choose a 1:X ratio that complements very well with the Pivot Points.

📈Heikin Ashi Based Entries:

Heikin Ashi entries are trades that are calculated based on Heikin Ashi candles but their price is executed to Japanese candles, thus avoiding false results that occur in Heikin candlestick charts, this making in certain cases better results in strategies that are executed with this option compared to Japanese candlesticks.

📊Dashboard:

A more visual and organized way to see the results and necessary data produced by our strategy, among them we can see the dates between which our operations are made regardless if you have activated some time filter, usual data such as Profit, Win Rate, Profit factor are also displayed in this panel, additionally data such as the total number of operations, how many were gains and how many losses, the average profit and loss for each operation and finally the maximum profits and losses followed, which are data that will be very useful to us when we elaborate our strategies.

Feel free to use this template to program your own strategies, if you find errors or want to request a new feature let me know in the comments or through my social networks found in my tradingview profile.

| Update 1.1 | | EN |

➕Additions: '

Time sessions filter and days of the week filter added to the time filter section.

Option to add leverage to the strategy.

5 Moving Averages, RSI, Stochastic RSI, ADX, and Parabolic Sar have been added as indicators for the strategy.

You can choose from the 6 available indicators the way to trade, entry alert or entry filter.

Added the option of ATR for Take Profit.

Ticker information and timeframe are now displayed on the dashboard.

Added display customization and color customization of indicator plots.

Added customization of display and color plots of trades displayed on chart.

📝Changes:

Now when activating the time filter it is optional to add a start or end date and time, being able to only add a start date or only an end date.

Operation plots have been changed from plot() to line creation with line.new().

Indicator plots can now be controlled from the "plots" section.

Acceptable and deniable range of profit, winrate and profit factor can now be chosen from the "plots" section to be displayed on the dashboard.

Aesthetic changes in the section separations within the settings section and within the code itself.

The function that made the indicators give inputs based on heikin ashi candles has been changed, see the code for more information.

⚙️Fixes:

Dashboard label now projects correctly on all timeframes including custom timeframes.

Removed unnecessary lines and variables to take up less code space.

All code in general has been optimized to avoid the use of variables, unnecessary lines and avoid unnecessary calculations, freeing up space to declare more variables and be able to use fewer lines of code.

| Lanzamiento Inicial | | ES |

Una actualización de mi antiguo script, este script está diseñado para que pueda ser usado como una plantilla para todos aquellos traders que quieran ahorrar tiempo al programar su estrategia y hacer un backtesting de ella, teniendo funciones ya programadas que en el desarrollo normal te tomaría más tiempo programar, con esta plantilla puedes simplemente agregar tu indicador favorito y así poder aprovechar todas las funciones que tiene esta plantilla.

🔴Stop Loss y 🟢Take Profit:

No hace falta mencionar que es un Stop Loss y un Take Profit, dentro de estas funciones encontramos las opciones de: porcentaje fijo (%), precio fijo ($), ATR, en especial para Stop Loss encontramos los Pivot Points, adicionalmente a esto, el rango de precio entre la entrada y el Stop Loss se puede convertir en un trailing stop loss, en cambio, especialmente para el Take Profit tenemos una opción para elegir un ratio 1:X que se complementa muy bien con los Pivot Points.

📈Entradas Basadas en Heikin Ashi:

Las entradas Heikin Ashi son operaciones que son calculados en base a las velas Heikin Ashi pero su precio esta ejecutado a velas japonesas, evitando así́ los falsos resultados que se producen en graficas de velas Heikin, esto haciendo que en ciertos casos se obtengan mejores resultados en las estrategias que son ejecutadas con esta opción en comparación con las velas japonesas.

📊Panel de Control:

Una manera más visual y organizada de ver los resultados y datos necesarios producidos por nuestra estrategia, entre ellos podemos ver las fechas entre las que se hacen nuestras operaciones independientemente si se tiene activado algún filtro de tiempo, datos usuales como el Profit, Win Rate, Profit factor también son mostrados en este panel, adicionalmente se agregaron datos como el número total de operaciones, cuantos fueron ganancias y cuantos perdidas, el promedio de ganancias y pérdidas por cada operación y por ultimo las máximas ganancias y pérdidas seguidas, que son datos que nos serán muy útiles al elaborar nuestras estrategias.

Siéntete libre de usar esta plantilla para programar tus propias estrategias, si encuentras errores o quieres solicitar una nueva función házmelo saber en los comentarios o a través de mis redes sociales que se encuentran en mi perfil de tradingview.

| Actualización 1.1 | | ES |

➕Añadidos:

Filtro de sesiones de tiempo y filtro de días de la semana agregados al apartado de filtro de tiempo.

Opción para agregar apalancamiento a la estrategia.

5 Moving Averages, RSI, Stochastic RSI, ADX, y Parabolic Sar se han agregado como indicadores para la estrategia.

Puedes escoger entre los 6 indicadores disponibles la forma de operar, alerta de entrada o filtro de entrada.

Añadido la opción de ATR para Take Profit.

La información del ticker y la temporalidad ahora se muestran en el dashboard.

Añadido personalización de visualización y color de los plots de indicadores.

Añadido personalización de visualización y color de los plots de operaciones mostradas en grafica.

📝Cambios:

Ahora al activar el filtro de tiempo es opcional añadir una fecha y hora de inicio o fin, pudiendo únicamente agregar una fecha de inicio o solamente una fecha de fin.

Los plots de operaciones han cambiados de plot() a creación de líneas con line.new().

Los plots de indicadores ahora se pueden controlar desde el apartado "plots".

Ahora se puede elegir el rango aceptable y negable de profit, winrate y profit factor desde el apartado "plots" para mostrarse en el dashboard.

Cambios estéticos en las separaciones de secciones dentro del apartado de configuraciones y dentro del propio código.

Se ha cambiado la función que hacía que los indicadores dieran entradas en base a velas heikin ashi, mire el código para más información.

⚙️Arreglos:

El dashboard label ahora se proyecta correctamente en todas las temporalidades incluyendo las temporalidades personalizadas.

Se han eliminado líneas y variables innecesarias para ocupar menos espacio en el código.

Se ha optimizado todo el código en general para evitar el uso de variables, líneas innecesarias y evitar los cálculos innecesarios, liberando espacio para declarar más variables y poder utilizar menos líneas de código.

Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2

This script was originally shared by Wunderbit as a free open source script for the community to work with. This is my second published iteration of this idea.

WHAT THIS SCRIPT DOES:

It is intended for use on an algorithmic bot trading platform but can be used for scalping and manual trading.

This strategy is based on the trend-following momentum indicator . It includes the Money Flow index as an additional point for entry.

This is a new and improved version geared for lower timeframes (15-5 minutes), but can be run on larger ones as well. I am testing it live as my high frequency trader.

HOW IT DOES IT:

It uses a combination of MACD and MFI indicators to create entry signals. Parameters for each indicator have been surfaced for user configurability.

Take profits are now trailing profits, and the stop loss is now fixed. Why? I found that the trailing stop loss with ATR in the previous version yields very good results for back tests but becomes very difficult to deploy live due to transaction fees. As you can see the average trade is a higher profit percentage than the previous version.

HOW IS MY VERSION ORIGINAL:

Now instead of using ATR stop loss, we have a fixed stop loss - counter intuitively to what some may believe this performs better in live trading scenarios since it gives the strategy room to move. I noticed that the ATR trailing stop was stopping out too fast and was eating away balance due to transaction fees.

The take profit on the other hand is now a trailing profit with a customizable deviation. This ensures that you can have a minimum profit you want to take in order to exit.

I have depracated the old ATR trailing stop as it became too confusing to have those as different options. I kept the old version for others that want to experiment with it. The source code still requires some cleanup, but its fully functional.

I added in a way to show RSI values and ATR values with a checkbox so that you can use the new an improved ATR Filter (and grab the right RSI values for the RSI filter). This will help to filter out times of very low volatility where we are unlikely to find a profitable trade. Use the "Show Data" checkbox to see what the values are on the indicator pane, then use those values to gauge what you want to filter out.

Both versions

Delayed Signals : The script has been refactored to use a time frame drop down. The higher time frame can be run on a faster chart (recommended on one minute chart for fastest signal confirmation and relay to algotrading platform.)

Repainting Issues : All indicators have been recoded to use the security function that checks to see if the current calculation is in realtime, if it is, then it uses the previous bar for calculation. If you are still experiencing repainting issues based on intended (or non intended use), please provide a report with screenshot and explanation so I can try to address.

Filtering : I have added to additional filters an ABOVE EMA Filter and a BELOW RSI Filter (both can be turned on and off)

Customizable Long and Close Messages : This allows someone to use the script for algorithmic trading without having to alter code. It also means you can use one indicator for all of your different alterts required for your bots.

HOW TO USE IT:

It is intended to be used in the 5-30 minute time frames, but you might be able to get a good configuration for higher time frames. I welcome feedback from other users on what they have found.

Find a pair with high volatility (example KUCOIN:ETH3LUSDT ) - I have found it works particularly well with 3L and 3S tokens for crypto. although it the limitation is that confrigurations I have found to work typically have low R/R ratio, but very high win rate and profit factor.

Ideally set one minute chart for bots, but you can use other charts for manual trading. The signal will be delayed by one bar but I have found configurations that still test well.

Select a time frame in configuration for your indicator calculations.

Select the strategy config for time frame (resolution). I like to use 5 and 15 minutes for scalping scenarios, but I am interested in hearing back from other community memebers.

Optimize your indicator without filters : customize your settings for MACD and MFI that are profitable with your chart and selected time frame calculation. Try different Take Profits (try about 2-5%) and stop loss (try about 5-8%). See if your back test is profitable and continue to optimize.

Use the Trend, RSI, ATR Filter to further refine your signals for entry. You will get less entries but you can increase your win ratio.

You can use the open and close messages for a platform integration, but I choose to set mine up on the destination platform and let the platform close it. With certain platforms you cannot be sure what your entry point actually was compared to Trading View due to slippage and timing, so I let the platform decide when it is actually profitable.

Limitations: this works rather well for short term, and does some good forward testing but back testing large data sets is a problem when switching from very small time frame to large time frame. For instance, finding a configuration that works on a one minute chart but then changing to a 1 hour chart means you lose some of your intra bar calclulations. There are some new features in pine script which might be able to address, this, but I have not had a chance to work on that issue.

Short Selling EMA Cross (By Coinrule)BINANCE:AVAXUSDT

This short selling script works best in periods of downtrends and general bearish market conditions, with the ultimate goal to sell as the the price decreases further and buy back before a rebound.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to to hodl this cash, or use it to reinvest when the market reaches attractive buying levels.

Entry

The exponential moving average ( EMA ) 20 and EMA 50 have been used for the variables determining the entry to the short. EMAs can operate better than simple moving averages due to the additional weighting placed on the most recent data points, whereas simple moving averages weight all the data the same. This means that price is tracked more closely and the most recent volatile moves can be captured and exploited more efficiently using EMAs.

Our backtesting data revealed that the most profitable timeframe was the 30-minute timeframe, this also enabled a good frequency of trades and high profitability.

A fast (shorter term) exponential moving average , in this strategy the EMA 20, crossing under a slow (longer term) moving average, in this example the EMA 50, signals the price of an asset has started to trend to the downside, as the most recent data signals price is declining compared to earlier data. The entry acts on this principle and executes when the EMA 20 crosses under the EMA 50.

Enter Short: EMA 20 crosses under EMA 50.

Exit

This script utilises a take profit and stop loss for the exit. The take profit is set at -8% and the stop loss is set at +16% from the entry price. This would normally be a poor trade due to the risk:reward equalling 0.5. However, when looking at the backtesting data, the high profitability of the strategy (93.33%) leads to increased confidence and showcases the high probability of success according to historical data.

The take profit (-8%) and the stop loss (+16%) of the strategy are widely placed to ensure the move is captured without being stopped out due to relief rallies. The stop loss also plays a role of mitigating losses and minimising risk of being stuck in a short position once there has been a fundamental trend reversal and the market has become bullish .

Exit Short: -8% price decrease from entry price.

OR

Exit Short: +16% price increase from entry price.

Tip: Research what coins have consistent and large token unlocks / highly inflationary tokenomics, and target these during bear markets to short as they will most likely have substantial selling pressure that outweighs demand - leading to declining prices.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

The backtesting data was recorded from December 1st 2021, just as the market was beginning its downtrend. We therefore recommend analysing the market conditions prior to utilising this strategy as it operates best on weak coins during downtrends and bearish conditions.

BlueFX Strategy We are re publishing the script so the Script Title doesn't display the old version number, to stop further confusion with our members.

This title will now remain constant, until you click into the strategy and the latest version number will be shown.

The previous release notes below are copied from the previous descriptions with the release note updates shown.

Hi Traders,

I hope everyone is great - its a long one - but worth the read, I promise....

Firstly, thank you to our members for being patient with this release - it took longer than anticipated but now with even more functionality too - and some improved profitability in back-testing on our H1 time frame especially - explained further below.

Secondly, thank you to the individuals that have made this happen - you know who you are! Sounds like an Oscar speech right.... sorry.

This tool we believe really does change the game - please read on to find out more.

As a brief reminder this builds upon on initial V1 and V2 indicator/scripts ...

The strategy itself

Our strategy will help you identify the current trend in the markets and highlight when this is changing. The strategy itself is based upon 4 indicators lining up in total confluence to increase the probability of the trade being a success.

Absolutely no technical analysis is needed to trade this successfully - this can be used on all time frames and all pairs - obviously with varying profitability as all pairs work differently - this can be reviewed quickly in 'Strategy Tester' to hone in on your own desired settings.

When all criteria is in alignment the strategy will convert all candles to the relevant colour - Green for an uptrend and Red for a downtrend; a candle that is printed normally simply shows that no current trend is in place to warrant a colour change. A normal coloured candle could possibly indicate a change in current market direction or the market consolidating before a further move in the initial direction.

When a new signal is valid, 'Blue FX Buy'' or 'Blue FX Sell' will be displayed and the small arrow shown on candle open for entry. (*Now along with Entry Price (EP), Stop Loss (SL), Take Profit (TP) and Lot size that is based on the risk parameters you have set personally on V3)

Version 2 was created with H4 confluence built in and also a display of a suggested Stop Loss (SL) and multiple Take Profits (TP's) on the H1 (One Hour) time frame - thus making your entry even easier and your SL more reliable - these suggested SL's and targets were based on the ATR of that pair at that time - a popular choice amongst traders - automatically built in.

What is a Trading View Script?

A script is like an indicator but better, we can prove the success of our strategy by using Trading Views strategy tester function. As shown below and on the chart - you can see the 'Buy' and 'Close Buy' on the chart, supported by a live trading log showing you the entry, entry price date, volume and closing price.

This is a great function for numerous reasons; firstly, you know you are using a profitable strategy, secondly you can use this as a trading journal to support your trading too. This in itself can help you with your trading psychology - letting winning trades run is a prime example of this. Take confidence in the statistics and performance over time.

Ultimately, we believe we have saved YOU the need to firstly, find an edge and a strategy - and all of the time it takes to BACKTEST a strategy - to then find it may or may not work - and then you start again!

Well guess what?

We know this works and it takes you seconds to see it.

Everyone can see the statistics themselves for 2020 to date (and previous!); an account gain of over 500% if you managed to catch all trades risking 1% per trade. I understand that catching all trades is difficult but even if you caught a third, that's still not too bad right?

Disclaimer alert; Please remember past performance is exactly that - how our strategy performed over those dates tested, it is not obviously a guarantee of future performance.

Even better, you/we can still hone in these settings to find an improved performance per pair on any given time frame and money management plan. (We are currently looking into automating this process too)

Default settings are set for use with the H1 time frame - no extra confluence checking is needed with these settings.

So what are the specific changes I hear you ask?

- Visibility of the SL and TP labels across all time frames.

- Visibility of all previous SL and TP labels with the click of a button (Prev. was only 2).

- Proof of the profitability of the strategy - we had this in V1 but this was based on trend following with the exit - we didn't in V2 when we added the SL and TP display function.

- The ability to customise the parameters and see the instant impact of the desired pair/time-frame and testing date range - of course some work better than others and will do at different times - once we have found a way to test this in an automated way we could look to do this monthly/quarterly to ensure we are using 'optimal' parameters at all times.

- Another game changer here is the addition of a lot size calculator - set your balance, set your risk and the LOT SIZE you should be trading will appear as if by magic - no need to use any other tool to do this. For inexperienced traders and especially trading stocks/ gold / commodities we suggest you check the contract sizes first as some brokers may operate differently. This visual cue will help ensure you are managing your risk and save you time in checking the right Lot Size for your trade (every pair has a different pip value and every trade a different SL).

- Although not required in our H1 settings currently - we have added more higher time frame confluences - which can improve the profitability of different pairs on different time frames in testing.

- As our tool can be used across all instruments we have a pull down menu for Crypto/Metals/Stocks/ Commodities , etc.

- The option to also test fixed lot size or percentage - see the benefit of compounding right away.

- The option to turn the testing function on and off.

Let's see an example......

An example trade - display Entry, SL, multiple TP, lot size and contract size.

snapshot

We have deliberately set the TP3 to be an increased target, this way we can capitalise on a large move in the market, should the move reverse and the opposite signal appears we close the trade anyway and follow the new signal.

I am unable to add other pictures in this Script description - but we will include in our Public channel and update our website to show them over the coming days.

I hope you can all see the functionality in this tool, the profitability in historic tests and how it can be used to give you your edge.

How do you access this I hear you ask?

Please visit our website for signup / purchase information in the first instance (the link is on our trading view profile / signature) or send us a private message on here - its impossible to keep track of comments on our posts so to ensure we don't miss you, a private DM will be great please.

Thank you for reading, we hope you choose to join our vastly growing community.

Kind regards

Darren

Blue FX

Jun 14

Release Notes: Default settings have been improved, providing a 600% gain YTD in back testing with less trades too.

Jul 4

Release Notes: Trend filter using ADX - our strategy is based on a trending market, adding the ADX filter to our strategy allows us to remove trades under the threshold level set. Previously - we tried to teach our members how to spot the ranging markets to help further increase their successes (although the stats were not based on any manual intervention) - now they don't have too.

Specific parameters set into the code - detects the pair and TF to shown them automatically - our method has been solid YOY growth based on a fixed 0.01 lot size to gain consistent yearly consistent results.

Trade volumes substantially reduced with a much higher win rate - due to the specific parameters and ADX filter.

No pull down menu when flicking between instruments - all done automatically; making it easier for trades flicking between trading instruments.

More TP options for testing - we have TP1/2/3 and other variables including FT (Follow Trend) / FT + SL (Follow trend with Stop loss) / TS (Trail Stop function)

Smaller labels showing entry, SL and TP, etc - much clearer on screen and on your app.

Lot sizes fixed - we had a previous bug affecting some currencies - as always where money is involved and managing risk, ensure you check and are comfortable this is correct of course

Filter for days of the week - some pairs hate specific days, a great tool, see how removing Fridays affects the performance in seconds.

Back testing on all instruments - not previously available - trade stocks like Tesla or Lloyds - or indices? We can give you back testing data for them all.

Filter for trading sessions - like the days of the week - if you are only trading London and US sessions, back testing data for other sessions is pretty pointless - now you can remove them too!

If you wish to just stay with the default V3 settings its simple, turn 'Use pre-defined parameter?' Off - and turn off ADX - your chart will then look like the initial v3.0 strategy anyway. However, every pair has improved performance we have found when including ADX - each pair is affected differently with a higher or lower ADX Threshold - this is parameter #9.

I don't think there is much more that can be added now - fuelled by our ambition - to provide our members with an easy yet profitable trading strategy for both beginner or experienced trader. We have this at the forefront of our minds when adding and reviewing functions.

Follow the trades, stay disciplined and don't focus on the money. Focus on the 'process' of following the strategy, its much easier on your mind too. Far easier following instructions than trying to do something without - follow your plan, the process and the money will follow.

If you wish to see all of the back testing data for each pair - hop into our Discord Server and check out the #public-backtesting-channel - all of them will be there when I post them tonight.

Jul 5

Release Notes: Another quick update.

More days of week added - Sat and Sunday trading sessions - (Sat - just crypto is open on TV)

Also a specific setting for trading just a certain time of day - this is based on EST time you will will need to convert back to your time zone for this to work.

For example, if you would like to test trading EURUSD between 7am and 11am - you will need to find the EST time for this which is 2am to 6am, you will then see these trades in the list of trades section. This is ideal for scalping certain sessions where all trades will be open and closed promptly.

I use the 'Time Buddy' app for this as its quite straight forward.

Regards

Darren

18 hours ago

Release Notes: Update - correcting the entry price label error.

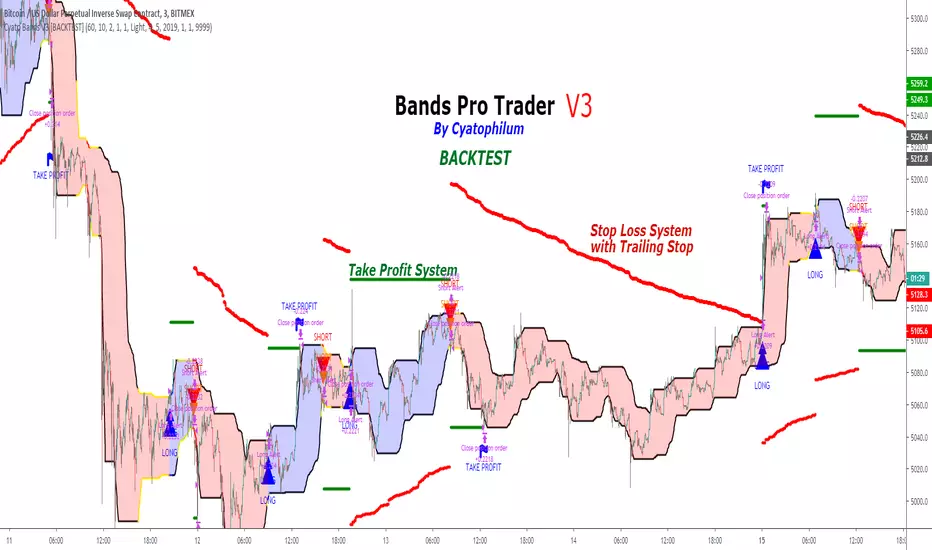

Cyatophilum Bands Pro Trader V3 [BACKTEST]An Original Automated Strategy that can be used for Manual or Bot Trading, on any timeframe and market.

>> Presentation <<

How it works

No, these are NOT Bollinger Bands..

The Cyatophilum Bands are an original formula that I created. You will probably never find it anywhere else.

Their behavior is the following:

When they are horizontal it means the trend is going sideways and they represent supports (lower band) and resistances (upper band).

When they are climbing or falling it means the trend is either bullish or bearish and they represent Trend Lines.

The strategy enters Long on a Bull Breakout and enters Short on a Bear Breakout.

The exits are triggered either on a Trend Reversal, a Stop Loss or a Take Profit.

FEATURES

Take Profit System

Stop Loss System

Show Net profit Line

More features here

Finding a profitable configuration is GUARANTEED

0. Choose your symbol and timeframe. Then add the Backtest version to your chart. If at any time you decide to change your timeframe, go back to step 1.

1. Open the strategy tester and look at the buy & hold line.

If it is mostly climbing (last value greater than 0) then it means we are in a bull market. You should then opt or a long only strategy.

If it is mostly dropping (last value lower than 0) then it means we are in a bear market. You should then opt or a short only strategy.

Note : This first step is really important. Trading against the market has very little chances to succeed.

2. Go into the Strategy Input Parameters:

check "Enable Long Results" and uncheck "Enable Short Results" if you are in a long only strategy.

check "Enable Short Results" and uncheck "Enable Long Results" if you are in a short only strategy.

3. Open the Strategy Tester and open the Strategy Properties.

We are going to find the base parameters for the Bands.

The "Bands Lookback" is the main parameter to configure for any strategy. It corresponds to how strong of a support and resistance the bands will behave. The lower the timeframe, the higher lookback you will need. It can move from 10 to 60. For example 60 is a good value for a 3 minute timeframe. Try different values, and look at the "net profit" value in the Overview tab of the Strategy Tester. Keep the Lookback value that shows the best net profit value.

Then play with the "Bands Smoothing" from 2 to 20 and keep the best net profit value.

The "Band Smoothing" is used to reduce noise.

Usually, the default value (10) is what gives the best results.

From this point you should already be able to have a profitable strategy (net profit>0), but we can improve it using the Stop Loss and the Take Profit feature.

4. To activate the Stop Loss feature, click on the "SECURITY" checkbox

You should see horizontal red lines appear.

A Long/short exit alert will be triggered if the price were to cross this line. (A red Xcross will appear)

Choose the Stop Loss percentage.

On top of that, you can enable the feature "Trailing Stop". It will make the red line follow the price, at a speed that you can configure with the "Trailing Speed" parameter.

Now, sometimes a stop is triggered and it was just a fakeout. You can enable "Re-entries after a stop" to avoid missing additional opportunities.

5. To activate the Take Profit feature, click on the "TAKE PROFIT" checkbox

You should see horizontal green lines appear.

A Long/short exit alert will be triggered if the price were to cross this line. (A flag will appear)

Choose the Take Profit percentage.

A low takeprofit will provide a safer strategy but can reduce potential profits.

A higher takeprofit will increase risk but can provide higher potential profits.

6. Money Management

You can configure the backtest according to your own money management.

Let's say you have 10 000 $ as initial capital and want to trade only 5%, set the Order Size to 5% of Equity.

You can increase net profit by increasing the order size but this is at your own risk.

How to create alerts explained here

Sample Uses Cases

Use it literally anywhere

This indicator can be used on any timeframe and market (not only cryptocurrencies).

About the Backtest below

The Net Profit (Gross profit - Gross loss) is calculated with a commission of 0.05% on each order.

No leverage used. This is a long strategy.

Each trade is made with 10 % of equity from an inital capital of 10 000$. The net profit can be bigger by increasing the % of equity but this a trader's rule to minimise the risk.

I am selling access to all my indicators on my website : blockchainfiesta.com

To get a 2 days free trial, just leave a comment , thanks !

Join my Discord for help, configurations, requests, etc. discord.gg

Crypto Scalping Strategy by SAIFOverview

An optimized scalping strategy designed for cryptocurrency markets, focusing on breakout opportunities with strict risk controls and optional safe compounding features. This strategy combines price action, volume analysis, and multi-timeframe trend confirmation.

Key Features

Breakout Detection System

Identifies significant price breakouts using dynamic channel analysis

Confirms breakouts with volume surge validation

Filters trades based on multi-timeframe trend alignment

Multi-Timeframe Trend Confirmation

Analyzes 1-hour and 4-hour timeframes for trend direction

Only takes trades aligned with higher timeframe trends

Uses long-term moving averages for trend validation

Advanced Risk Management

Conservative default risk: 1% per trade

ATR-based stop-loss placement (2x ATR)

Trailing stop mechanism to protect profits

Minimum profit target before trailing activates

Built-in position sizing based on account equity

Safe Capital Management Options

Fixed Capital Mode: Trade with consistent position sizes

Safe Compounding Mode: Gradually scales position size based on realized profits only

Drawdown Protection: 80% equity floor prevents excessive capital erosion

Leverage Control: 10x leverage factored into position calculations